SMM News on June 23:

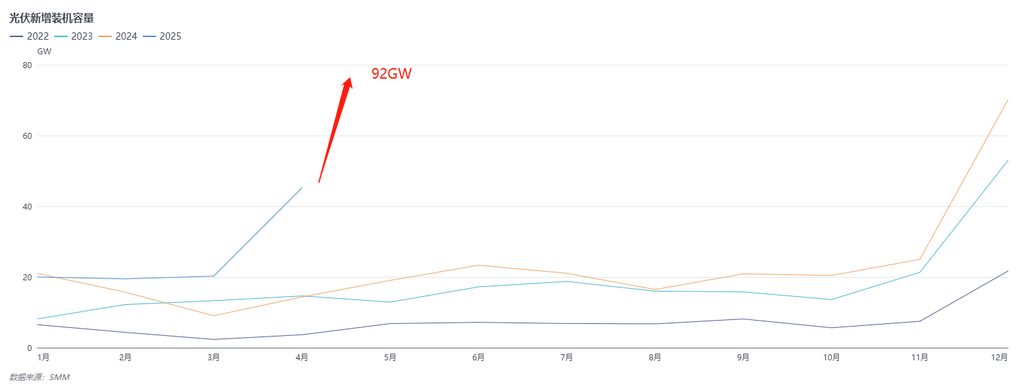

On the 23rd, the National Energy Administration (NEA) announced China's new PV installations in May. Data showed that in May 2025, domestic PV installations reached approximately 92 GW, up 383.2% YoY and over 100% MoM, hitting a new record high for the same period in history. Domestic new PV installations totaled 197.85 GW, up 150% YoY.

Meanwhile, overseas export demand also saw unexpected growth. Customs data indicated that PV module exports in May were estimated at 22.7 GW, up 0.9% YoY and 2.8% MoM. Cumulative exports from January to May reached 109.23 GW, down 2.2% YoY.

Why did domestic demand exceed expectations with such significant increases?

From the perspective of domestic new installations, the substantial growth in May was mainly influenced by the "531" policy. As the last month for existing projects, distributed projects rushed to complete installations in May.

For overseas markets, the growth in exports was primarily driven by the approaching summer peak electricity demand period, with rigid demand for electricity in Southeast Asia, Africa, and other regions driving market installations.

Considering the stockpiling cycle, domestic module prices also basically reached their peak for the year by the end of March and early April. Taking the price of N-type 183 modules as an example, the price in early April was approximately 0.78 yuan/W, up about 11.9% from the low point in H1 2025.

Regarding expectations for Q3, SMM believes that the installation rush at the end of Q2 has, to a certain extent, significantly consumed market demand in H2. The overall pressure from the demand side in H2 may be relatively large. Currently, SMM expects that the lowest point for monthly installations in the Q3 2025 market may fall back below 20 GW, and expectations for the peak installations at the end of the year are low, with monthly installations possibly not exceeding 40 GW. Meanwhile, regarding the prices of subsequent main materials, SMM believes that even by the end of the year, it will be difficult to surpass the price peaks in H1.

》View SMM's PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)